From the beginning, we baked in tight feedback loops:

-

In-app feedback prompts after key actions

-

Weekly interviews with power users and churned users

-

UserTesting.com scripts for onboarding and AI interactions

-

Surveys on emotional trust and friction

Examples of Iteration:

-

Switched reminder language from “Pay Now” to “Just a Heads Up” after testing tone sensitivity

-

Removed auto-splits on first use — too jarring; added preview before execution

-

Simplified AI chat with less finance jargon after testing comprehension rates

Results

-

14,000 users on waitlist onboarded in 9 weeks

-

65% week-over-week retention

-

10,000+ of 1:1 convos used to shape features

-

Users report feeling less stressed, more “in sync” financially

-

$1M in venture capital raised to support the project

-

Accepted into Google for Startups

-

Accepted into NVIDIA’s AI Program

Product Strategy & Reflections

Peas didn’t just need to be a good product it had to be trustworthy, invisible, and emotionally calibrated to manage joint money journeys. That set the bar higher than most consumer fintech products. Here’s how I anchored the product strategy blow past that bar.

1. Designing for the Modern Relationship, Not the “Joint Account”

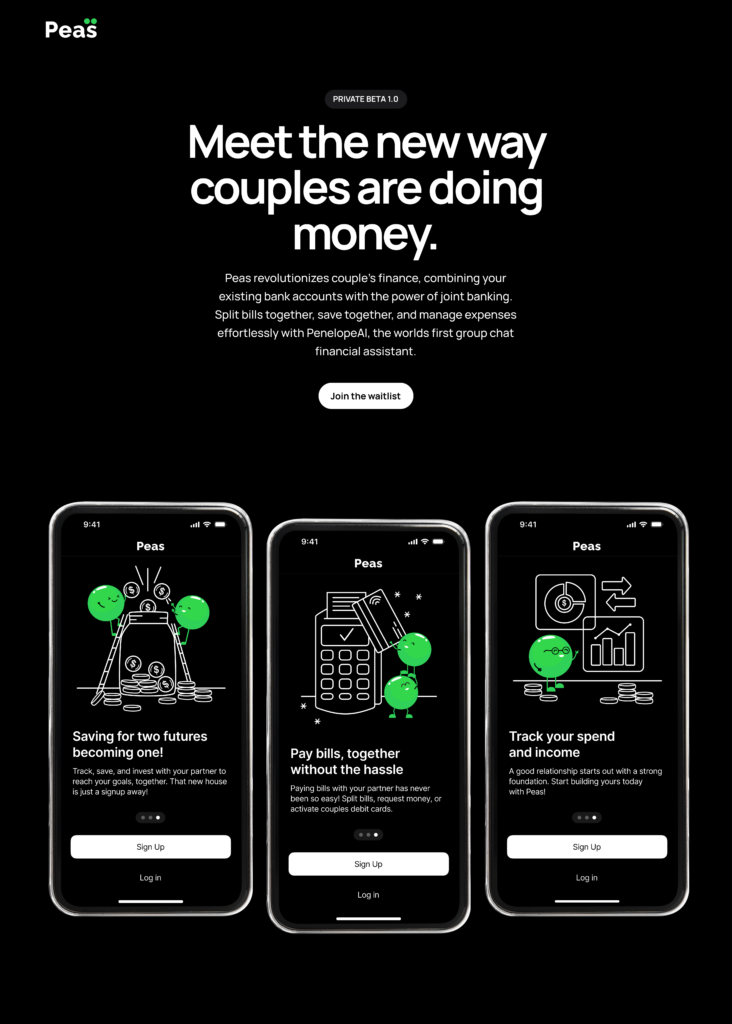

A fundamental decision we made early was to decouple our product from the outdated metaphor of joint banking. Most existing solutions, from Chase joint accounts to Venmo, assume shared finances; which means shared accounts. But 75% of our ICP actively avoids those tools due to complexity and bottle necks. What they wanted wasn’t shared money, it was shared understanding of that money.

So we defined our architecture around “collaborative autonomy”:

-

Shared visibility, but separate accounts

-

Mutual decisions, but no forced merges

-

Joint control, but granular privacy

This was a strategic design wedge. It let us serve Gen Z and Millennial users who live together, raise kids together, and split lives together without forcing them to change how they feel about money. Even applying to secondary and tertiary personas like Roommates and Families.

The product’s edge wasn’t that we built better features. It was that we built for a different emotional premise.

2. Creating a Product-Led Retention Loop with the Subscription Value Loop

From the beginning, we designed Peas to grow through usage. Marketing is great, but real retention comes from viral loops and users needed to share our product with others.

-

Value Creation: Provide clarity, fairness, and emotional ease from day one (i.e., “This helped us finally talk about money without arguing.”)

-

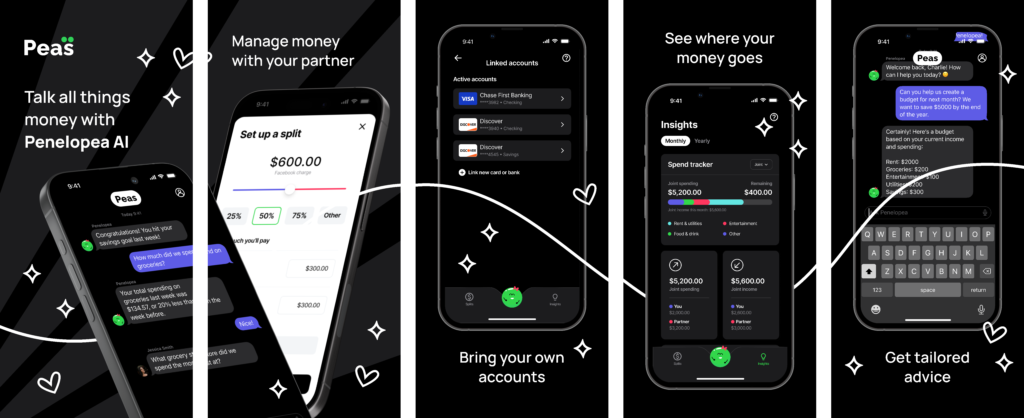

Value Delivery: Fast onboarding, seamless linking (Plaid, Finicity, MX), and just-in-time nudges from PenelopeAI

-

Value Capture: Introduce meaningful subscription layers only after we deliver a real “money relationship OS”

By focusing first on how often a couple interacts with the product, we drove strong retention and had low churn during our first launch. For a consumer subscription app, hitting 65% week-over-week retention was a rare sign that we were in the right emotional lane.

Instead of tracking just DAUs or MAUs, we tracked shared moments per week per pod as well as frequency of conversation. This was our north star for relational stickiness and helped us prove that using natural language to manage money was the proper direction.

3. Emotional UX as a Product Strategy Lever

Traditional fintech often forgets this.. but language is part of money. How we communicate about it, how we learn about it, even how we plan with it.

We wanted to test every word for emotional friction. From call-to-actions (“Pay Now” → “Just a Heads Up”) to AI phrasing (“You spent more” → “Your contribution looks higher than usual — want to rebalance?”).

This was to create a system of trust. Money is inherently stressful and confusing. Every surface of the product, text, timing, and tone, became a lever that shapes whether couples could trust us and more importantly, just our AI.

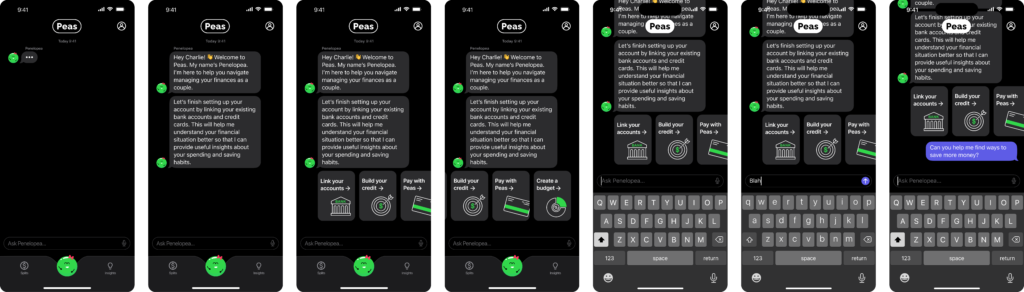

This also impacted how we scoped the chatbot. PenelopeAI’s suggestions were designed to offer insights without accusation and at the right times in the money journey.

We treated emotional trust as a tier-one KPI. That’s what made Peas feel like a friend, not a finance tool. Something the best experiences are doing well in the new age of AI powered tools.

4. Sequencing for Trust: From Visibility → Mobility → Intelligence

Most products try to do too much too fast. We deliberately sequenced Peas as a trust-ladder:

-

Step 1: Visibility – show joint data without judgment

-

Step 2: Mobility – enable equitable, flexible movement (splits, pods, joint approvals)

-

Step 3: Intelligence – introduce PenelopeAI as a liaison to the couple

We thought AI should enter a relationship like a good therapist; by listening first, providing value second, and offering solutions later.

5. Intentional Tradeoffs Around Simplicity vs. Power

Peas walks a delicate line between financial tooling and emotional safety. We intentionally rejected overbuilt features that sounded “smart” but felt too intrusive. Some of the tradeoffs:

-

No auto-split on first use (felt aggressive)

-

Preview + confirmation flows (earned trust first)

-

No pushy subscription walls (we actually removed the paywall after initially seeing friction on activation)

-

Delayed monetization in favor of building usage-based value

We asked ourselves often: Would this make a user feel more in sync or more managed?

That became our internal litmus test for feature decision making.